It’s no secret that all African countries are net importers of pharmaceutical products. A Brookings report claims that, as of 2019, in the $14 billion sub-Saharan African pharma market, 70 to 90% of drugs consumed were imported. As for vaccines, the picture isn’t much rosier – Africa accounts for 25% of global vaccine demand but only 0.1% of vaccine production.

For decades, governments, homegrown manufacturers, and international pharma companies have tried to fortify local pharma production in Africa. The African Union (AU) and the Africa Centres for Disease Control and Prevention (Africa CDC) aim to produce 60% of Africa’s vaccine demand domestically by 2040. The Covid-19 pandemic provided much-needed momentum to this endeavour; it highlighted that local pharma production in Africa is non-negotiable. From import dependence, African countries are now moving towards more regionalised supply chains; pharmaceutical exports from Africa are a natural extension of this trajectory.

The African pharmaceuticals industry

As the global population grows and standards of living increase, the demand for pharmaceutical drugs, vaccines, equipment, and supplies is growing worldwide. In Africa, too, the double burden of communicable and non-communicable diseases is driving demand for African pharmaceuticals. The United Nations Economic Commission for Africa (UNECA) reckons that African industries have the potential to respond to this demand. A 2021 report by the UN agency highlights how local pharma and medical product manufacturing in Africa took a new shape in the face of the pandemic. South Africa’s U-Mask switched from producing protective masks for mining and agriculture to medical respirator masks; Nigeria’s National Agency for Science and Engineering Infrastructure made the first indigenous ventilators; separately, Senegal and Ghana made strides in diagnostics. Global vaccine manufacturers like Moderna and BioNTech also entered deals to build mRNA vaccine production facilities.

Local pharma production in Africa will have to happen at multiple stages of the value chain, including R&D, API manufacturing, bulk manufacturing, fill-and-finish, and packaging. But the benefits of local pharma production in Africa make the endeavour more than worth it. Pharmaceutical self-sufficiency will lead to improved health outcomes, reduced dependence on foreign stakeholders, and economic resilience. The economic benefits will come from reduced import costs, low labour costs, foreign direct investment, and exports to different countries. Increased investments in pharma and medicine exports from Africa will further propel skilled labour development, robust regulatory systems, and scientific and technological innovation. These factors will only make pharmaceutical exports from Africa more attractive.

Compared to countries like India and China, which have more developed pharmaceutical industries, African pharmaceuticals manufacturers still have some way to go. In 2019, McKinsey categorised the pharma industry development stage of most sub-Saharan countries as “sizeable” at most. But even these sizeable industries have emerging export bases. Kenya, Nigeria, and South Africa earned mention as the most notable pharma producers in SSA.

Leveraging local pharma production in Africa

The McKinsey research revealed the benefits of local pharma production in Africa. It also noted the spillover effects of localisation on increasing pharmaceutical exports from Africa.

For starters, the costs of pharma products. At present, it is cheaper to import drugs from countries like India. However, with the right infrastructure, comparable plants could produce cost-competitive or even cheaper medications in future. This possibility is particularly promising for relatively simple drugs like oral solids. Even for tablets, capsules, creams, and certain other products, the costs of production in Ethiopia and Nigeria are often about 5 to 15% lower than landed import prices from India. For many other SSA countries, this scenario is still theoretical. Nonetheless, with higher capacity and utilisation rates, this could very well become a reality.

Economically, the benefits of local pharma production are estimated to be about $190 million for Ethiopia and $230 million for Nigeria annually by 2027. This is a modest contribution to the countries’ overall GDP, but it would have a significant effect on the balance of trade. Increasing their shares of local pharma manufacturing from 15-20% to 40-45% could help each country improve their trade balance by $150 million to $200 million annually.

Ultimately, increased local pharma production in Africa would have a positive impact on drug regulation and quality assurance. For instance, in Ethiopia, a push for domestic manufacturing was accompanied by the strengthening of the national drug regulator. This was reflected in commitments to reduce product registration delays, crack down on counterfeit drugs, and enforce certain standards of pharma quality. These measures push pharma manufacturers in the country to produce export-quality drugs, which meet international standards.

Pharma exports from African countries

The continent may be largely import-dependent, but pharma exports from Africa are far from a pipe dream; in fact, African exports are already playing an emerging role in global pharmaceutical chains. The value of pharmaceutical exports from Africa has increased steadily in recent decades. In 1998, African pharmaceuticals export totalled $0.2 billion in value; by 2018, that number had increased to $1.4 billion. UNECA reckons this indicates the potential to further expand local pharma production and medicine exports from Africa.

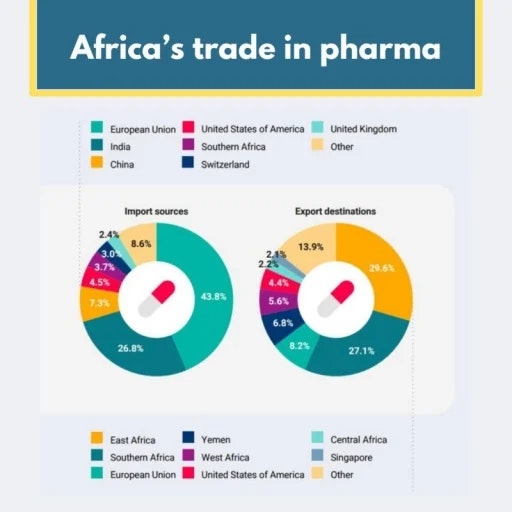

A Brookings commentary from 2021 points out that medicine exports from Africa tend to stay within Africa. Over half of African pharmaceuticals exports go to East and Southern Africa, with the remaining going to Europe, Yemen, the United States, Singapore, and other countries within and beyond Africa. Meanwhile, UNECA averaged data from 2016 to 2018 to find the leading intra-African importers and exporters of medicinal and pharmaceutical products by value. Senegal, Tanzania, Zimbabwe, Zambia, Sudan, and Uganda comprised the top 6 importers. The list of top intra-African exporters, on the other hand, was populated by South Africa, Kenya, Ghana, Egypt, Morocco, and Tunisia – the first four of these countries account for nearly 70% of intra-African pharma exports.

Outside of Africa, the top sources of African pharma imports were the EU27, India, Switzerland, China, the USA, and the UK. Beyond continental boundaries, the leading destinations for pharmaceutical exports from Africa were the EU27, the USA, Saudi Arabia, Yemen, and the UK. Optical, medical, and surgical instruments also form a significant proportion of Africa’s health sector exports. When classified according to end use under the system of national accounts, consumption goods claim the lion’s share of African pharma exports with capital, and intermediate goods also contributing in no small measure.

An IQVIA whitepaper presents the export opportunities generated by localisation efforts in Egypt and Algeria. The pharmaceutical industry is an integral part of the Egyptian government’s Vision 2030, with localisation being a foundational aspect of it. In 2016, Egypt’s trade deficit was estimated to be $1.5 billion; by 2030, the country hopes to bring that down to $0. Several initiatives have been instituted to achieve this target, resulting in promising export opportunities for African pharmaceuticals. Such initiatives are increasing the number of local manufacturing plants with international GMP certification. Pricing incentives for exports and to circumvent complex local market challenges are also driving local manufacturing initiatives. Further, the government is facilitating the registration of new local generics for domestic and export markets.

Specifically, Egypt opened the Gypto Pharma City in Greater Cairo in 2021. The largest pharma city in the Middle East and Africa, Gypto manufactures 150 types of medicines across 160 production lines. It makes vitamins and drugs for Covid-19, chronic diseases, and other health conditions prevalent in the region. Its ambitions encompass localising new tech and manufacturing pharmaceutical raw materials. Gypto Pharma City is the ideal gateway to export pharma products to other African and Middle Eastern countries, making Egypt a regional hub.

Meanwhile, in Algeria, by strengthening industrial capacity and regulatory frameworks, localisation is expected to strengthen the case for local API production and increase regional exports. Already in 2018, Sanofi established the largest manufacturing and distribution facility in Africa here. This plant produces 100 million units across 25 products, including tablets, syrups, diabetes drugs, etc. (~80% of Algeria’s output) for distribution, sale, and export.

Transforming risks into opportunities

The Covid-19 pandemic shocked African localisation efforts into renewed action. At least 30 vaccine manufacturing projects have been announced across 14 countries to supplement existing facilities. But with this estimated increase in capacity comes the need for better coordination.

A report by the Wellcome Trust and Boston Consulting Group (BCG) points to the risk of overcapacity for certain products. Some of these risks have already been averted by halting or repurposing projects. But where they still exist, risks can be transformed into opportunities.

The existing and announced capacity for vaccine fill-and-finish is likely to be over 60% greater than the target for 2040. This translates to about 2.2 billion excess doses annually. For specific drug substance (DS) manufacturing, meanwhile, current and announced capacity will double the target for 2040, should all announced plans materialise. Should all the pharma products manufactured here be headed for local markets, there is a risk of wasted investments and cannibalisation among manufacturers. However, with appropriate coordination and transparency, this excess capacity can cater to export markets, establishing the important contribution of African pharmaceuticals to the global market.

In this regard, African governments and regional organisations ca n learn from countries like India. India’s Pharmexcil – the government agency that promotes external trade by organising international trade delegations, buyer-seller meetings, and international seminars – boosts pharma exports by sharing important information and opportunities. What Pharmexcil did for the Indian pharma industry on the global stage, an equivalent entity in Africa can do for African pharmaceuticals. Already, there are crucial initiatives like the African Medicines Agency (AMA), the African Medical Supplies Platform, and, of course, the African Continental Free Trade Area (AfCFTA) that aim to coordinate and simplify regulatory systems and trade across boundaries on the continent.

The AfCFTA

The African Continental Free Trade Area (AfCFTA) is a free-trade agreement that offers an opportunity to boost intra-African trade. UNECA posits that the AfCFTA can help build more resilient African pharmaceuticals industries, especially when it comes to the trade of pharmaceutical intermediates. Some modalities of the pan-African agreement commit ratifying AU Member States to eliminating at least 90% of tariff lines on goods imported from other parties to the AfCFTA over a period of 5 to 15 years. It will also be important for Member States not to include essential health sector goods like ventilators, medicines, and personal protective equipment (PPE) from exclusion lists.

At present, where local pharma producers are involved, they play a limited role in the overall value chain. But post-Covid strides in African pharmaceuticals show that that scenario could change. As local pharma production in Africa gets a boost, so do medicine exports from Africa. Localisation depends on regulatory system strengthening, quality assurance, competitive pricing, tech transfers, and skill development – all of these elements will also make African pharmaceuticals more attractive on the global stage. At the end of the day, Africa’s emerging role as a pharma exporter is one to look out for. With the right infrastructure, demand forecasting, and strategic partnerships, African pharmaceuticals exports will be a force to reckon with.

Sources:

- “Figure of the week: Africa’s trade in pharmaceuticals”, Brookings, 9 December 2021“

- "Building competitive and resilient pharmaceutical value chains through the African Continental Free Trade Area”, UN Economic Commission for Africa, June 2021“

- "Localization of Pharmaceutical Manufacturing in Middle East and North Africa Region”, IQVIA, May 2022“

- "Should sub-Saharan Africa make its own drugs?”, McKinsey, 2019“

- "Scaling up African vaccine manufacturing capacity”, Wellcome, January 2023

This post has been researched and written exclusively for Pharmaconex Egypt by our Editorial Partner, TheKable.news

Supporting Partners

Media Partners